ALLiS Login |

(877) 254-4429

(877) 254-4429

ALLiS Login |

(877) 254-4429

Fourth Quarter 2022

NEWS YOU CAN USE FROM THE EXPERTS AT LLIS

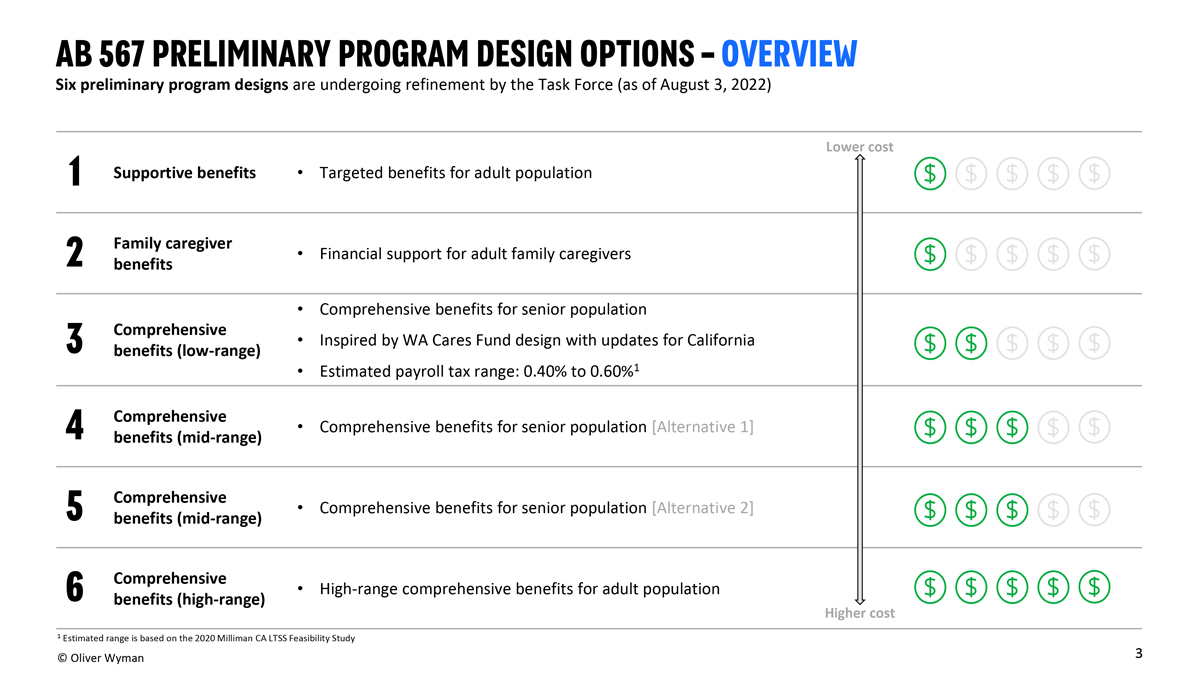

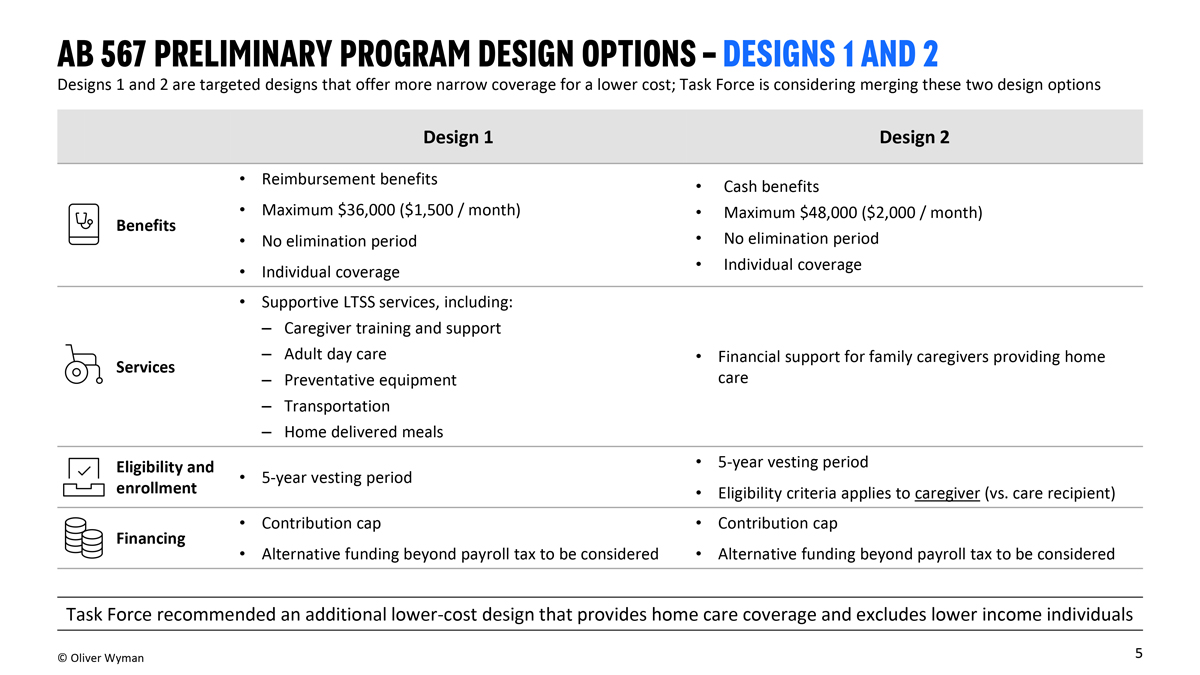

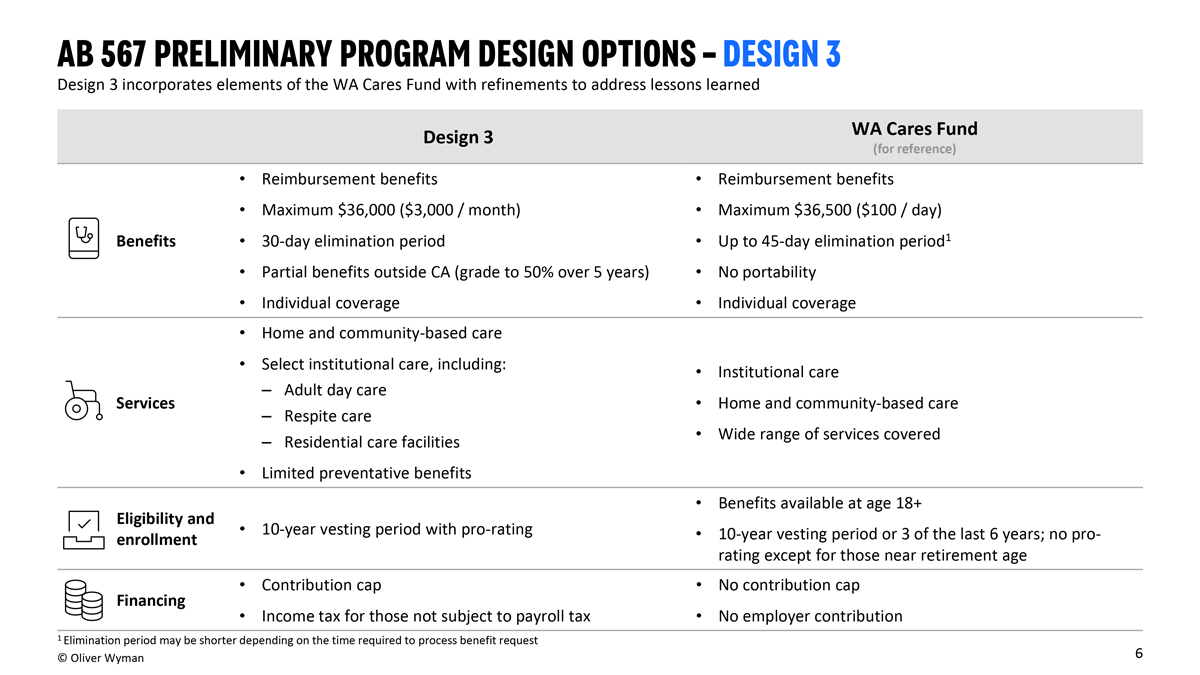

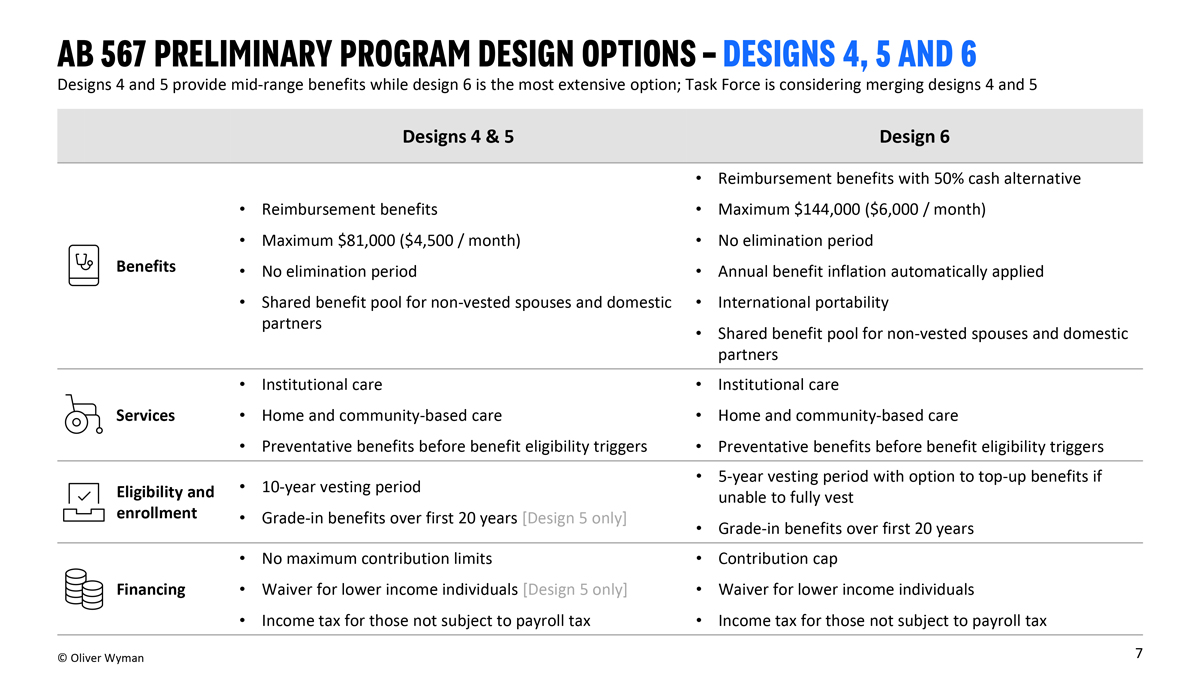

The California Long Term Care Insurance Task Force’s preliminary recommendations for a state LTC program (funded by payroll taxes) are expected to be finalized prior to January 1, 2023.

No matter what the fine print holds, your youngest clients with the highest incomes may pay the most tax (initial estimates in the .40-.60% range; the existing Washington state plan was .58%) for the longest time if/when the program is established.

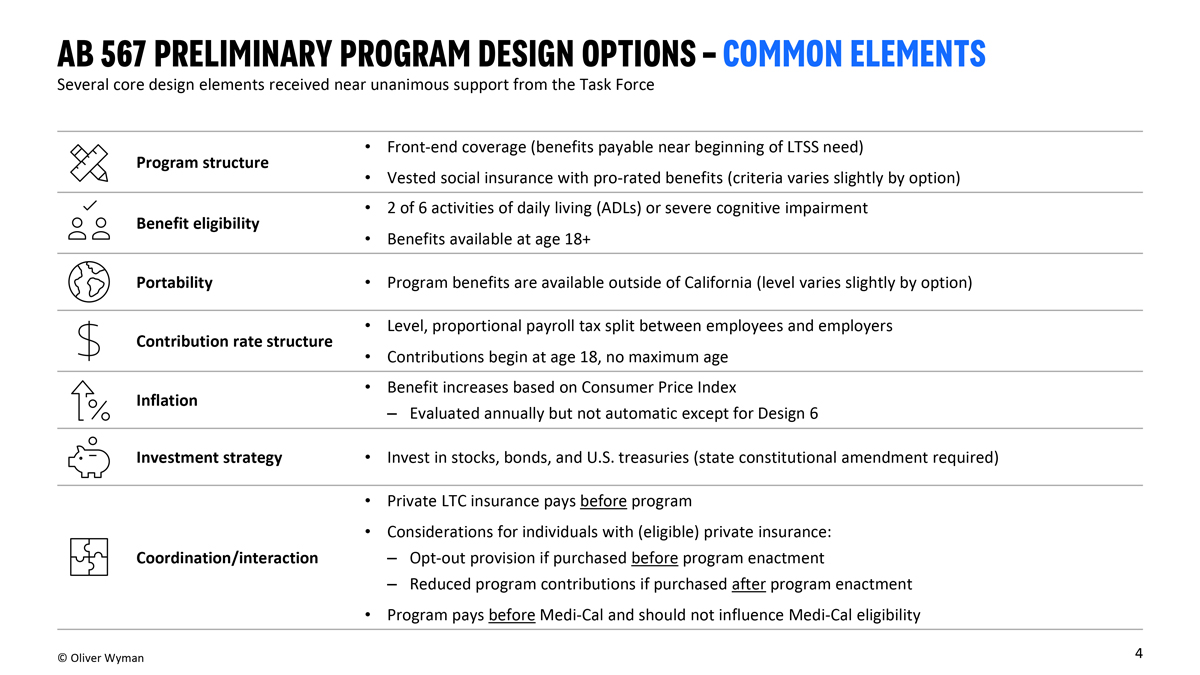

Other state LTC program proposals provide for an opt-out provision for employees covered by private LTC plans, so CA is expected to offer this, but timing is the issue:

Gave advance notice and allowed clients months to apply before new rules kicked in

Gave advance notice and allowed clients months to apply before new rules kicked in

Proposed opt-out period ends the date of the enactment

Proposed opt-out period ends the date of the enactment

Requires qualified coverage in force for one year prior to the enactment of the program

Requires qualified coverage in force for one year prior to the enactment of the program

WA had almost 5 times the projected number of people apply to opt out, so the industry expects any opt-out period for all other programs to be short/non-existent.

Talk to your young/high-income clients today about LTCi as “Payroll Tax insurance.” The first thing insurance companies did to stem the tide on applications was to raise the minimum age for new applications. Next was raising the minimum premium/policy benefit before turning the spigot off completely in WA.

Approximately 480,000 out of the 3,800,000 employees (13%) opted out of the Washington Cares Fund by having (or recently applying for) qualifying LTCi coverage. This nearly broke the LTCi industry (not just the insurance companies but examiners, medical records retrieval firms, third-party phone interviewers), leaving a lot of people without time or options to obtain personal coverage to opt out of the payroll tax.

CA has approximately 16,500,000 employees.

Click here to view the full pdf.

Jill MacNeil, LLIS’s LTCi expert, is here to help you and your CA clients.

SOLUTIONS AVAILABLE THROUGH LLIS

Term Life Insurance | Low-Load Universal Life (Individual & Survivorship) | No Lapse Guaranteed Univeral Life (Individual & Survivorship) | Long Term Care Insurance | Disability Insurance | Critical Care Insurance | Low-Load Variable Annuity | Immediate and Fixed Annuities | Low-Load Variable Universal Life | Hybrid Life/LTCi | Hybrid Annuity/LTCi

(We recommend low-load permanent life insurance and annuities when possible)

(Not all policy types available in all states)

For a list of current providers, visit the Advisor Tools section of our website and click on "Insurance Companies We Work With".