ALLiS Login |

(877) 254-4429

(877) 254-4429

ALLiS Login |

(877) 254-4429

Fourth Quarter 2022

NEWS YOU CAN USE FROM THE EXPERTS AT LLIS

We sent this on September 21 via email, but think it’s important enough to share with you again, or for the first time if you missed that email.

The Long Term Care insurance (LTCi) industry thought California might be the next state (after Washington state last year) to bring an LTC bill to a vote (CA’s state LTC Taskforce hopes for a feasibility report by 1/1/2023 and an actuarial report by 1/1/2024), but it looks like Pennsylvania or New York may beat them to it!

NY Senate Bill S9082 and PA House Bill HB2779 create an LTC trust program to provide LTC benefits for eligible residents and collect premium contributions from all state employees via income tax withholding.

Will they pass?

- PA: The Democrat-sponsored bill is currently in committee, but Republicans control the Senate and House.

- NY: Another Democrat-sponsored bill, but Dems control both House and Senate, so arguably a better chance of passage than PA.

What do you and your clients need to know?

From our readings, opt-out periods (time to request an exemption from the payroll tax by already holding qualifying LTC coverage) will be short to non-existent. WA state’s extended opt-out period allowed almost one-half million people to apply for exemptions. WA budgeted for only 105,000 opt-outs, so that’s 400,000 fewer paychecks to tax, hurting the long-term feasibility.

PA and NY may have learned from this. PA may not give any warning when the program goes into effect, and NY ups the stakes with a one-year lookback period for exemption eligibility!

PA Opt-Out: One short, somewhat open-ended section: Exemption.--An employee who demonstrates that the employee has LTC insurance is exempt from the premium assessment under this section.

The payroll tax amount is undetermined, but since PA plans to use WA state as the benchmark, it would be .58% of income (uncapped) for a $100/day benefit for 365 days. NY plans benefits are similar at $36,500 for one year, but the tax is undetermined.

NY Opt-Out: Provides an optional exemption for individuals who have had private LTC insurance in place continuously for at least the duration of the calendar year to date prior to the effectiveness of the law, for as long as they maintain those policies.

If the plan goes into effect in 2024 (consensus on the earliest start date from industry watchers), clients must be insured for all of 2023, so they will have to purchase a policy before 12/31 of this year!

What do you and your clients need to know TODAY?

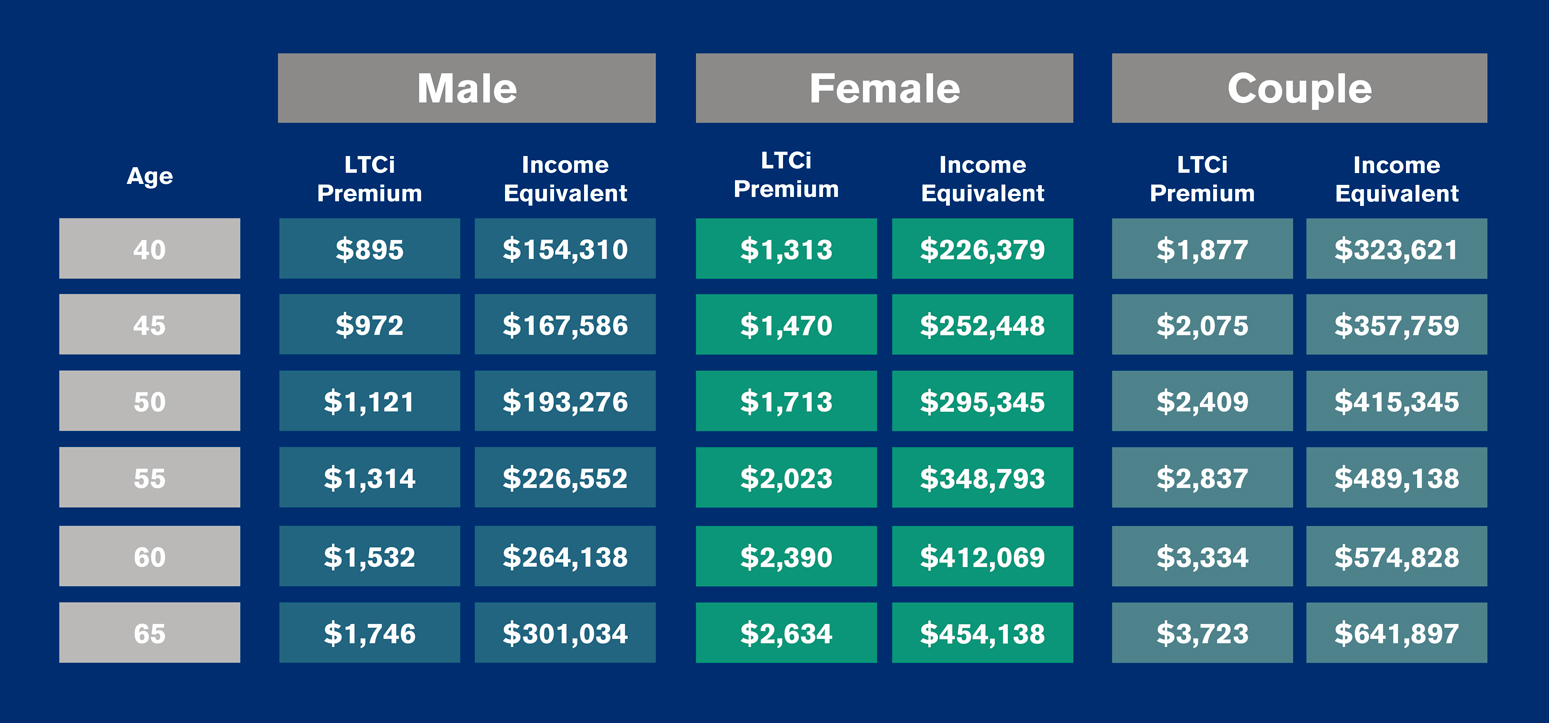

If/when the bill becomes law, your clients may not have enough time to apply. And higher-income clients will pay the most tax. Clients with incomes exceeding the below income equivalents would pay less in LTC premiums than what the tax might be. Forewarned is forearmed, so discuss the benefits of a personal LTCi policy with your high-income earners now because a non-capped tax will hit them hardest!

Jill MacNeil, LLIS’s LTCi expert, is here to help you and your PA and NY clients.

SOLUTIONS AVAILABLE THROUGH LLIS

Term Life Insurance | Low-Load Universal Life (Individual & Survivorship) | No Lapse Guaranteed Univeral Life (Individual & Survivorship) | Long Term Care Insurance | Disability Insurance | Critical Care Insurance | Low-Load Variable Annuity | Immediate and Fixed Annuities | Low-Load Variable Universal Life | Hybrid Life/LTCi | Hybrid Annuity/LTCi

(We recommend low-load permanent life insurance and annuities when possible)

(Not all policy types available in all states)

For a list of current providers, visit the Advisor Tools section of our website and click on "Insurance Companies We Work With".